Customer engagement in financial services: real-world examples that work

Published on April 09, 2026/Last edited on April 09, 2026/11 min read

Team Braze

82% of financial services companies say their customers are satisfied with their messaging experience, but only 41% of consumers agree.

This rather big gap between perception and reality suggests that somewhere between sending a message and it actually landing, financial services brands are losing the thread—and the most likely reason is a failure to truly understand the people on the other end.

These are customers sharing their most sensitive data: income, spending patterns, long-term financial goals. Openness like this carries an expectation with it that the brand will use that information to be genuinely useful, to show up in moments that matter. When messaging misses that mark, it feels like noise to the customer, and in a sector built on trust, this has consequences.

The brands featured here have each found a way to move closer to what their customers want and need. Here's how they did it.

What is customer engagement in financial services?

Customer engagement in financial services is how brands build and maintain meaningful relationships across the entire customer lifecycle, from the first onboarding step through to long-term retention and product expansion.

Strong engagement programs are built on first-party behavioral data and respond to what customers actually do. They coordinate across channels—email, push, in-app messages, SMS, WhatsApp—so every interaction feels connected and coherent. This makes customers feel understood at each stage of their financial journey rather than marketed at.

Types of customer engagement in financial services

Customer engagement in financial services spans a wide range of actions—from lightweight signals like opening a push notification, to high-intent behaviors like completing a credit application or activating a savings offer. Each signal tells you something different about where a customer is in their journey, and what they're likely to need next.

Not every signal carries the same weight. A push open tells you someone was reachable. A first deposit tells you something clicked. Building engagement triggers around the signals that reflect real intent—rather than just activity—is what separates programs that drive retention from those that just drive noise.

Why does financial services engagement demand a different approach?

Financial services customers are making high-stakes, often emotionally charged decisions—and they expect brands to recognize that in every interaction. When someone is navigating a credit application, opening a savings account, or making their first investment, the communication they receive either supports that moment or gets in the way. Add regulatory requirements that govern what can be said, to whom, and how, and the margin for a poorly conceived message narrows considerably.

Most industries can absorb a degree of generic marketing. Financial services has very little tolerance for it. Yet the Braze 2025 Financial Services Customer Engagement Review found that only 41% of financial services companies personalize messages based on real-time engagement signals like clicks and views—the lowest rate of any surveyed industry. Brands that don't respond to live behavioral data are essentially guessing. In financial services, guessing can be a particularly costly habit.

The case studies that follow show what a more customer-led approach looks like and what it produces.

Real-world customer engagement examples in financial services

The four brands below operate in very different markets—from Canada to Latin America, from micro-investing to digital banking—but they were each dealing with a version of the same problem: customers who weren't getting the right message at the right moment. Here's what they did about it.

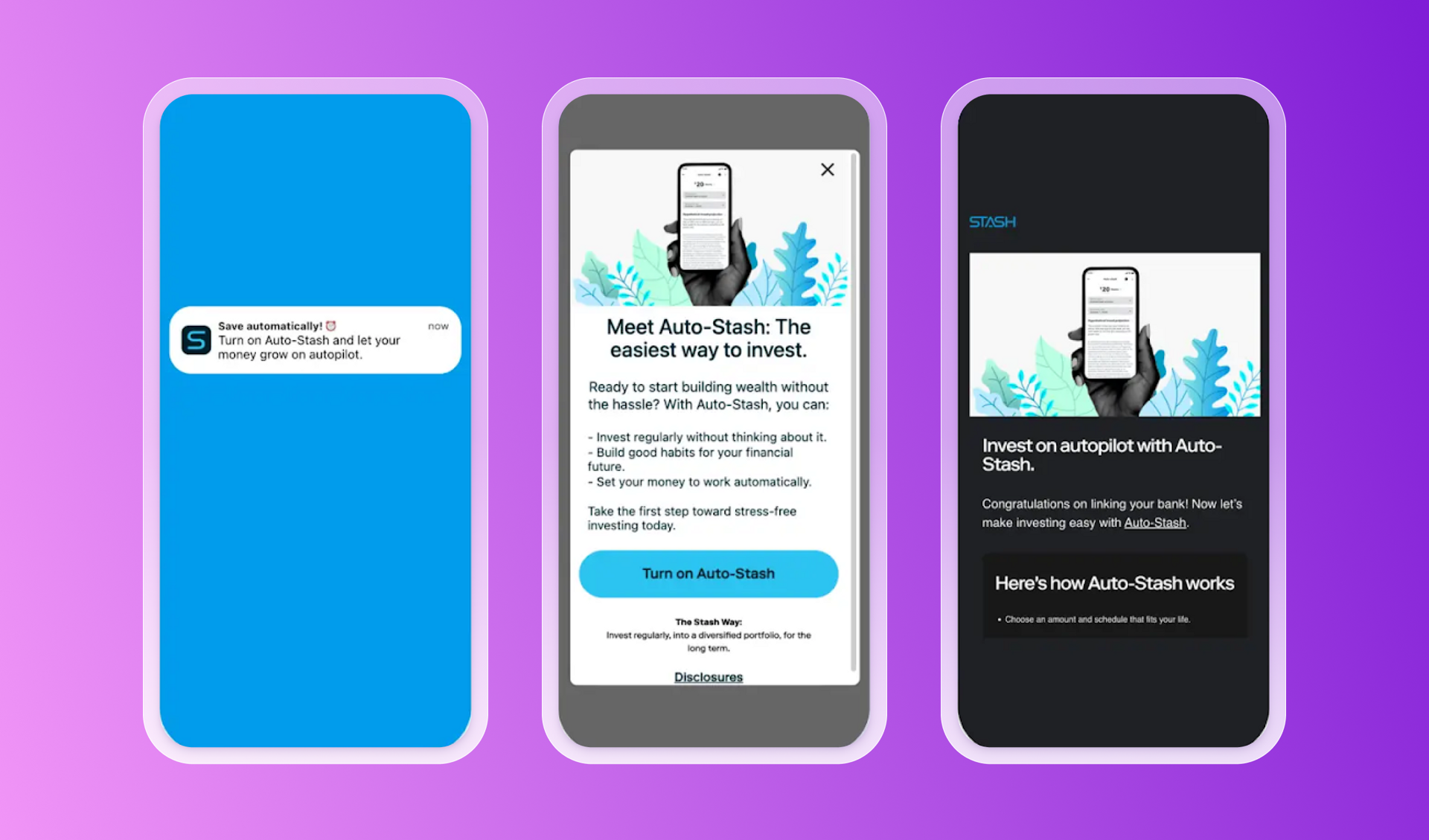

Stash invests in onboarding

Stash is a micro-investing platform on a mission to make investing accessible and affordable for everyday Americans. With a user base that includes many first-time investors, building confidence early is the difference between a user who activates and one who disappears before making their first deposit.

The challenge

Stash's onboarding funnel had multiple steps, and users were dropping off at different points for different reasons. A single, linear onboarding journey couldn't address the specific hesitations of each individual and in a trust-dependent, regulated industry, a poor first experience rarely gets a second chance.

The strategy

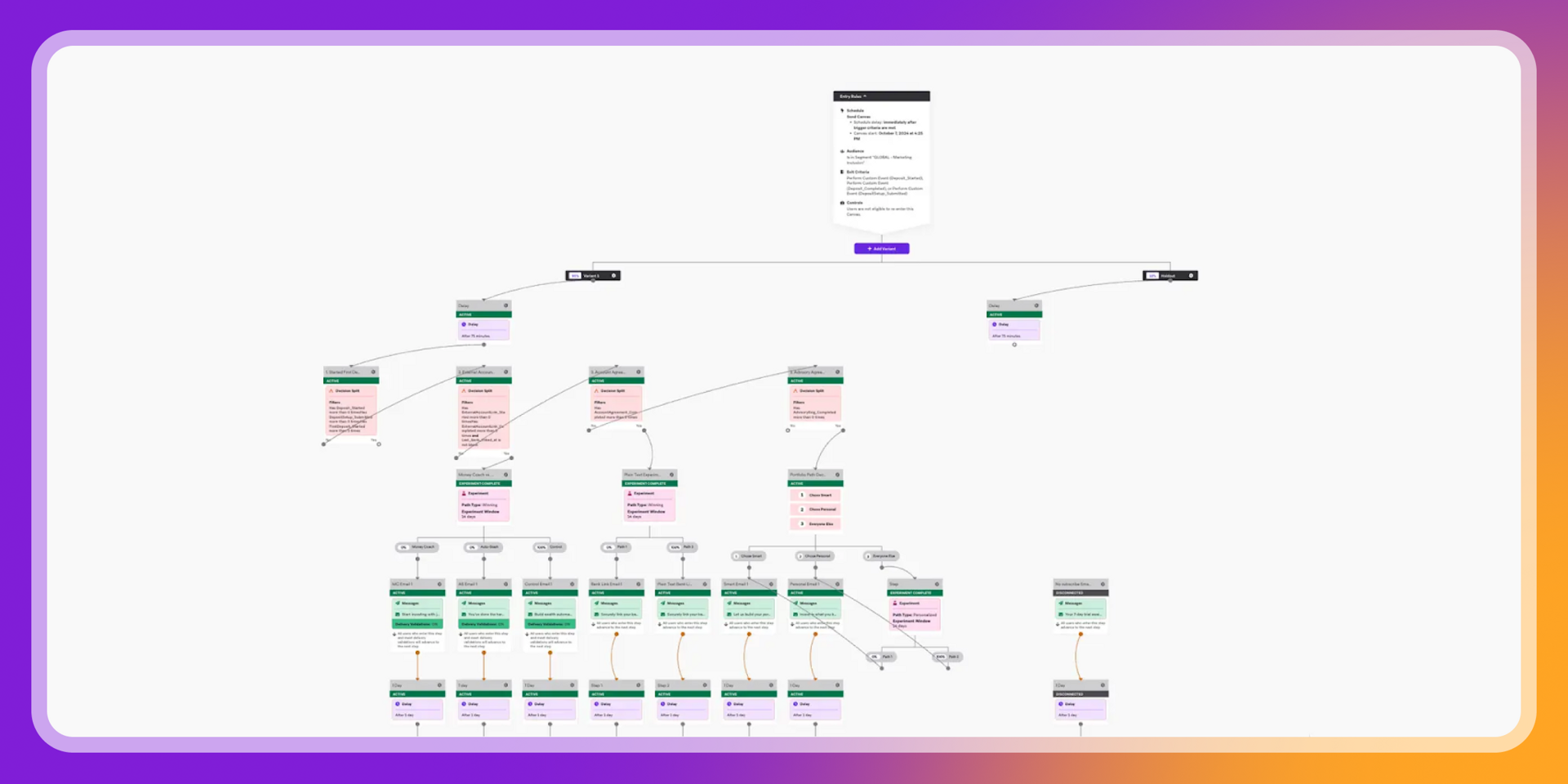

Using Braze, Stash built a multi-Canvas onboarding campaign that used real-time segmentation and behavioral triggers to identify exactly where in the funnel a given user had stopped, then delivered messaging that spoke directly to that moment.

Rather than restarting the conversation from scratch, the campaign picked up where the user had left off, highlighting the features and benefits most relevant to their next step. Messages ran across email, push, in-app, and SMS in combination.

The wins

- 72% increase in email open rates

- 64% increase in email click-through rates

- 20.34% increase in conversion rate for FirstDeposit_Started

- 18.71% increase in conversion rate for DepositSetup_Submitted

- 19.75% increase in conversion rate for Deposit_Completed

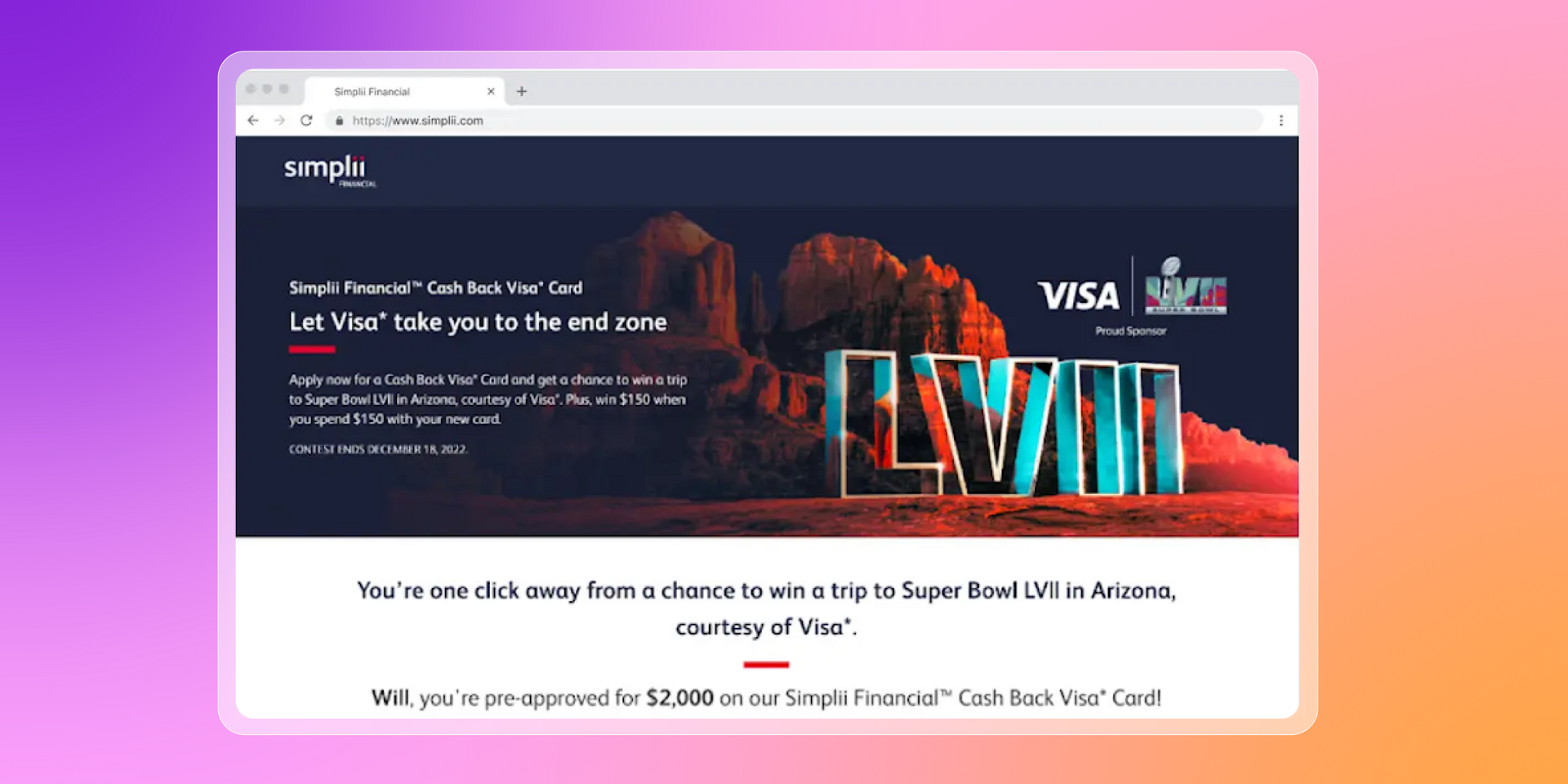

Simplii's “One Click Credit” campaign scores big

Simplii Financial is a digital-only bank serving around 2 million Canadians with no-fee banking, credit, mortgages, and investments. A division of CIBC, Simplii's proposition is built on making banking straightforward—no monthly fees, no unnecessary complexity.

The challenge

Customers eligible for pre-approved credit card offers were still entering their own details manually, adding unnecessary steps and losing conversions along the way. Simplii's Digital Distribution Channel campaigns were also being managed through an internal system that limited their ability to personalize at scale.

The strategy

Switching to Braze, the team launched the "Simplii Super Bowl One Click Credit" campaign: A personalized, pre-approved offer that eligible customers could accept with a single click.

Using Connected Content and Liquid, Braze pulled each customer's details directly into the message, removing manual data entry entirely. Eligible customers received customized offers through in-app messaging and email only, with a $150 bonus incentive and the chance to win a trip to Super Bowl LVII in Arizona.

The campaign took over five weeks to build, but created a foundation that reduced future campaign execution to two weeks or less.

The wins

- Campaign execution time reduced from 5-plus weeks to two weeks or less

- Close to 30,000 credit cards dispatched over three years through the campaign

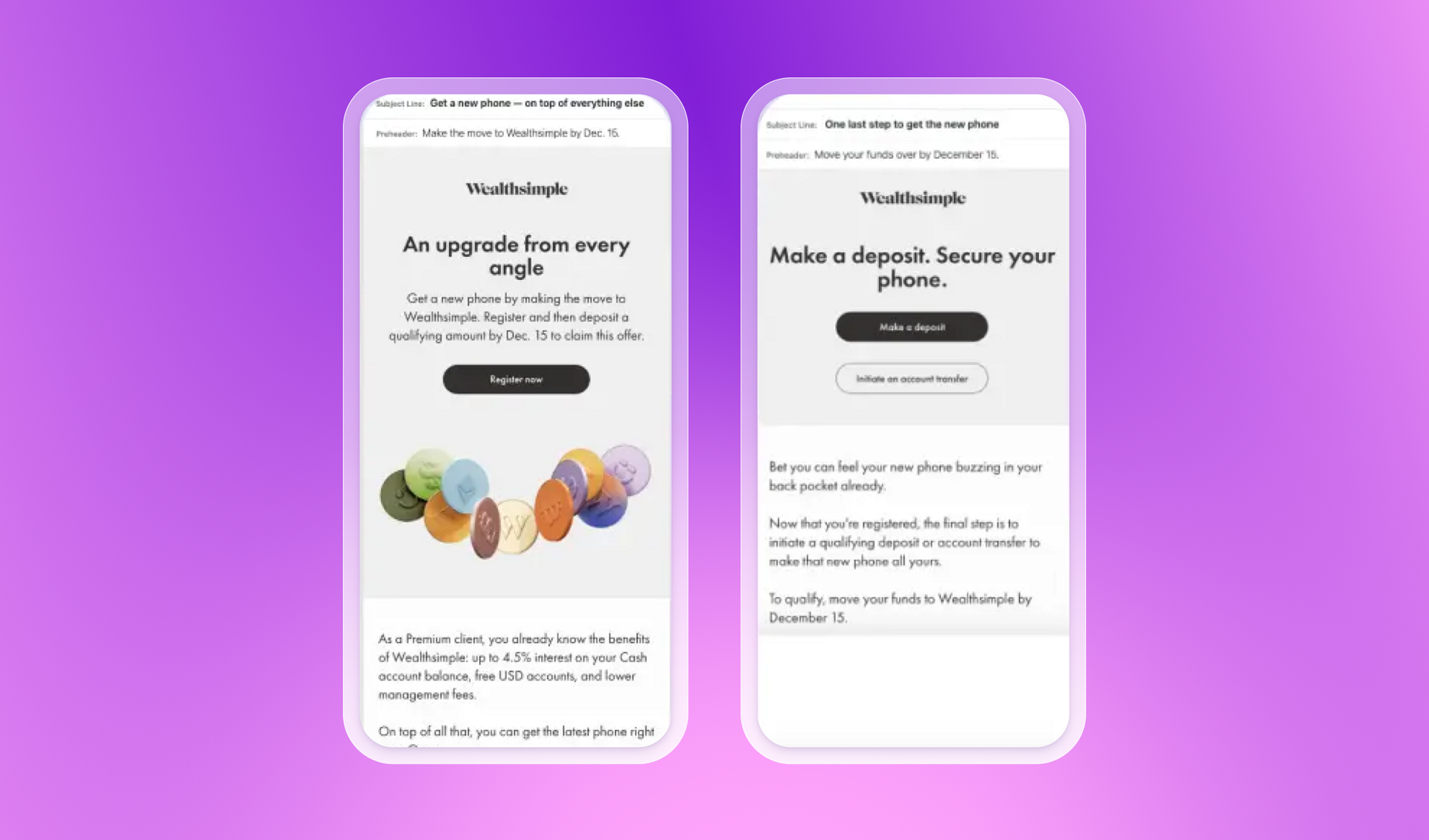

Wealthsimple makes it count: one campaign, record deposits, 25% new clients

Wealthsimple is one of Canada's fastest-growing money management platforms, serving over 3 million Canadians and managing over $30 billion in assets across investing, cryptocurrency, tax filing, and more. Its ambition extends beyond product—it wants to be its clients' primary financial relationship.

The challenge

Before moving to Braze, Wealthsimple had the data to support personalized, automated campaigns, but lacked the platform capability to act on it. The team needed a scalable solution that would let them address every stage of the customer journey without heavy engineering involvement in each campaign build.

The strategy

Wealthsimple launched a campaign to encourage both new and existing clients to move their financial assets to the platform by offering a straightforward incentive: A cell phone for clients transferring a qualifying amount of assets.

Using emails, in-app messages, and Content Cards, the team collected registrations and sent confirmation messages with detailed next steps. Braze Data Transformation passed client registrations from an external source and automatically added custom attributes to each user profile on completion.

The campaign's tone leaned into transparency, which was a deliberate contrast to the promotions more typical of traditional banking.

The wins

- 40% increase in team quarterly net deposits, including a record-breaking month

- 20% of clients who received the campaign registered for the promotion

- 25% of all participants were new clients, making it as effective for acquisition as it was for retention

Stori flips the script on payment reminders with WhatsApp

Stori is a fintech operating across Latin America with a mission to extend financial inclusion to people underserved by traditional banking. With a 99% credit acceptance rate and a product built hand-in-hand with its users, Stori's engagement strategy starts from a straightforward premise: listen to customers, identify their pain points, and fix them.

The challenge

Several of Stori's customer processes were creating unnecessary friction—particularly around address updates for card replacements and payment reminders. Previous WhatsApp providers were unreliable at scale and lacked the journey orchestration tools needed to run personalized campaigns properly.

The strategy

After switching to Braze, Stori launched two WhatsApp campaigns. For card replacements, customers could update their address directly within a WhatsApp message with a single click. For payment reminders, Stori used Canvas to orchestrate an interactive chatbot experience, passing customer data and quick reply responses from Braze to their chatbot tool via webhooks and Liquid logic.

What had been a potentially stressful notification became a personalized, two-way exchange complete with fun facts. Amplitude, a Braze Alloys partner, handled analytics and ongoing optimization throughout.

The wins

- 3x more engagement with WhatsApp compared to push notifications

- 26% higher conversion on address updates compared to the in-app process

- Significant uplift in overall conversion rates alongside improved customer retention

How do financial services brands use data to engage customers in real time?

Financial services brands use real-time data by mapping customer moments to behavioral signals, then responding with the next best experience across the right channel at the right time.

A moment could be a new user stalling at a key onboarding step, a customer becoming eligible for a pre-approved offer, or someone making their first deposit. The signal is the data point that confirms it, like a session drop-off, an eligibility flag, or a conversion event. The experience is whatever comes next, like a behavioral nudge, a personalized offer, or a confirmation message that reinforces confidence.

The case studies above show this playing out across very different contexts. What connects them is the same underlying discipline—behavioral data activating a specific response, at a specific moment, on the channel most likely to reach that customer.

What should financial services customer engagement software actually do?

The right financial services customer engagement software connects customer data to real-time action—ingesting behavioral signals, updating segments as new data comes in, and firing the right message across the right channel without manual intervention. It handles the complexity of cross-channel orchestration, regulated communications, and personalization at scale, so marketing teams can focus on strategy rather than execution.

You can see it in the numbers from the brands above. Simplii reduced campaign execution from five weeks to two. Wealthsimple's team moved faster without engineering bottlenecks. Stori launched complex WhatsApp flows without writing code. Better engagement and leaner execution arrived together.

Lani Ha, Marketing Manager at Acorns, describes Braze as "an incredible career accelerant.” One of her standout projects involved using Liquid Logic to dynamically personalize content based on customer insights.

What metrics matter most for measuring customer engagement in financial services?

The metrics that matter most for financial services customer engagement are those tied directly to customer behavior over time: activation rates, retention, session frequency, conversion events, and lifetime value. Open rates and send volume tell you whether messages were received—behavioral metrics tell you whether they worked.

Activation and onboarding conversion: Track whether new customers complete the steps that lead to real product usage like a first deposit, a linked account, or an activated card. These early events are strong predictors of long-term retention, which is why Stash's focus on FirstDeposit_Started as a primary conversion metric was so deliberate. Hitting 20.34% on that event, across nearly 60,000 users, is what meaningful activation looks like.

Retention and session frequency measure whether customers continue to engage with a product over time. Braze data shows that cross-channel messaging produces meaningful uplift in six-month retention for financial services brands—reflecting the value of staying consistently present across multiple touchpoints rather than relying on a single channel.

Conversion and revenue impact show whether engagement is driving real value. Wealthsimple's 40% increase in quarterly net deposits and record-breaking month weren't marketing metrics—they were business outcomes that followed directly from a better engagement strategy.

Channel engagement metrics like click-through rates, in-app response rates, and WhatsApp interaction rates provide the feedback loop that allows teams to optimize journeys over time. Stash's 72% increase in email open rates and 64% lift in click-through rates, and Stori's 3x WhatsApp engagement rate versus push, were signals that the right message was reaching the right person at the right moment.

If you're building a measurement framework, keep the top line focused on retention and activation, then break out conversion and channel performance by segment and key lifecycle moments.

Common customer engagement mistakes in financial services

The same mistakes tend to show up across financial services engagement programs, regardless of the size of the brand or the sophistication of the team. Here's what to watch out for.

Measuring success by product adoption alone. Product adoption is a useful signal, but building an entire engagement strategy around it tends to produce messaging that feels like a sales pitch rather than a service—and customers notice.

Not testing engagement strategies. Without testing, there's no way to know whether a message is working because of its timing, its content, its channel, or something else entirely. Optimization becomes guesswork.

Personalizing on stale or overly broad segments. Jobs change, financial goals shift, life moves on—and suddenly messaging built on outdated segments reflects a customer who no longer exists. Refreshing segments off recent behavioral data is what keeps personalization feeling relevant.

Letting cross-team friction block personalization. Engagement strategy in financial services rarely sits with one team. When marketing, product, and IT operate in silos, the customer experience reflects that fragmentation.

Sending at the wrong moment. A relevant message at the wrong time is still the wrong message. Payment reminders that arrive after a due date, offers that land mid-onboarding, re-engagement campaigns that fire for customers who are already active—timing errors like these erode trust faster than generic messaging.

Related Tags

Releated Content

View the BlogCustomer engagement in financial services: real-world examples that work

Team Braze

Retail customer engagement: Real campaigns, real results

Team Braze

Introducing Smooth Operator, a new video series about BrazeAI Operatorᵀᴹ